Quantative analysis of BUMPER Finance

BUMPER FINANCE

Welcome, subscribers! Thank you for subscribing. What will be shared today and the days ahead are alpha from our Economics Design's researchers.

Please keep these mails secret and do not share them with any one because these alphas are confidential. Enjoy your reading.

TLDR below. This is not financial advice.

Disclaimer: We helped Bumper in the token modelling and recommended changes to improve the incentives.

General Conclusion

In this article, we analyse Bumper Finance shortly, by breaking down the fundamental drivers of the protocol, token supply, token demand and market activity.

First, we analyse protocol cash flow, in comparing to similar price protection protocols.

Secondly, we examine the token supply model, including creating an additional sigmoid function in token distribution.

Thirdly, given the various incentive policies designed by the Bumper team, we study and report on the internal demand function of the token.

Fourthly, we combine cash flow, token supply and dynamics of token demand analyses into a circulating supply analysis, giving two possible scenarios - ideal and reasonable.

Fifthly, we give our insights to the fully diluted value (FDV) analysis, as a proxy to the analysed performance of the token and ecosystem.

Finally, we provide some provide some insight into our some discussions and iterations we had, with the Bumper team which precipitated several enhancements given our insights, to improve accuracy of the model and analysis.

What Is Bumper Finance?

Bumper Finance is a DeFi price protection protocol built on Ethereum mainnet. Bumper provides a mechanism by which holders of the underlying asset can maintain the value of their position against a decline in the price of this asset in the market.

Bumper Finance works by transferring risk to the risk-taker (Maker) and receiving some income from the risk-averse party (Taker).

Bumper is a price insurance protocol.

Bumper’s Token Model

Bumper is a crypto asset price protection protocol. The assets include Ethereum and (wrapped) Bitcoin for their initial release, and this forms the basis of our analysis.

The core mechanism - price protection for Takers who pay premiums which are collectively earned by Makers - provides the incentives for Makers and Takers to transact with the protocol.

The native token of Bumper, $BUMP, is used as an access token which is required to be “bonded” (locked) with the protocol to take out a position. The required bond is calculated as a proportion of the $USDC value of the user’s position.

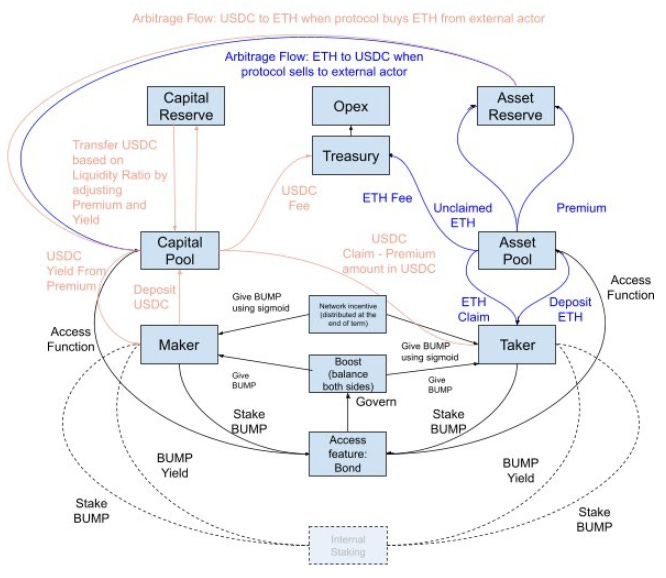

BUMP Value Flow Model

The black lines show the flow of $BUMP for takers and makers, the driver of internal demand.

The black dotted line shows the flow of $BUMP for staking, which can extend th3e mass public, who are not makers nor takers. This is a driver of speculative demand.

The pink lines show $USDC flow from the maker side. The blue lines show assets like $ETH and $wBTC from the taker side.

The underlying value of $BUMP is driven by: (1) total value locked (TVL) of the protocol, (2) token inflation, and (3) token demand arising from speculative and non-speculative aspects.

Simply, increasing TVL results in a general upward trend of $BUMP price. The fundamental driver of increasing TVL rests on the ability of the protocol to provide sufficiently attractive price protection for Takers and yields for Makers such that the protocol TVL increases over time, as well as macro activity affecting the prices of Ether and Bitcoin.

Cash Flow Forecast

TVL

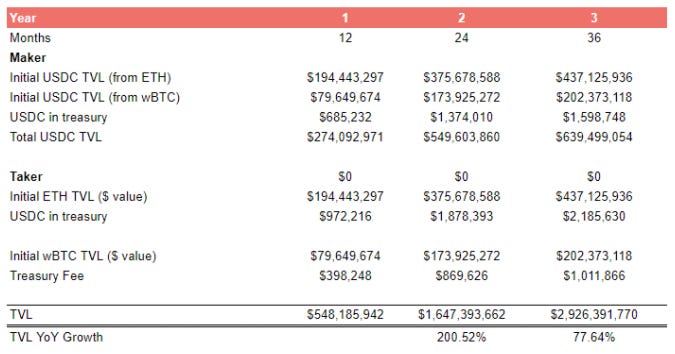

One of the main drivers of Bumper Finance’s cash flow forecast was the protocol’s TVL growth rate by comparing with other the DeFi Options and Insurance Protocols.

According to our analysis, the protocol TVL would reach $1b by month 18 and approximately $2.9b by the end of the three years. This is reasonable as the TVL in DeFi is at $100b , growing exponentially and the market capitalisation of $ETH and $BTC are $500b and $1tr respectively.

A year-over-year summary table is provided above which shows a total cumulative TVL of $548m, $1.6b, and $2.9b for years 1, 2, and 3 respectively, representing a 201% growth in year 2 and a 78% growth in year 3.

Treasury

The protocol charges a fee to Makers and Takers, at a 0.25% and 0.5% rate respectively. The funds are added to the treasury, to function as the tertiary protocol insurance. The treasury amount is in $USDC from Maker and $ETH or $BTC from Taker.

Throughout the three years, the model has forecasted an increase in the treasury amount. The trend in the data was expected: as the TVL increases, more Makers and Takers are taking positions of their assets and thus increase the fees earned by the protocol from providing the service.

In addition, at the end of the 3 years, we expected an split among the three asset classes, namely $ETH, $wBTC, and $USDC, with a higher proportion in $ETH relative to $wBTC due to its late introduction. Specific percentages of each asset class, after 3 years:

Token Supply Analysis

Bonding Curve And Network Incentives

The network incentive function in the Bumper protocol design is defined by the following Sigmoidal relation:

With:

a: 10,000,000

b is setted to 5(%) with a minium viable network effect size of $50m.

c: 50,000,000

The Bumper pattern defined by the equation on the right characterises the circulating supply of $BUMP (network incentive) in $USD as a function of $USDC TVL.

We also developed an additional sigmoid curve to simulate incentives in terms of newly released $BUMP as a function of the total dollar value of incentives:

A simplified network incentive model of:

The boost incentive as a percentage of TVL:

The specific parameters of the additional sigmoid function are given below:

In addition, we also have a "boost" incentives that is fixed to 2.72%. Additional tokens via the boost function are issued to incentivise $USDC deposit to return to the balance of assets in the protocol given the importance of $USDC in servicing Taker and Maker liabilities.

Token Emission Rate

Based on the incentive model presented above, we expect 65.8% of Total Supply to be issued as capital growth in the protocol. 80.6% through year 2 with an inflation rate of 22.5% and finally close to 90% in year 3 with an inflation rate of 11.3%

Specifically, with the above new distribution, the monthly inflation rate will decrease from 17% to 2% in the first 15 months and maintain a gradual decrease to 1% throughout the rest of the $BUMP distribution.

Hence, we have Cir. Supply over time as shown below:

Token Demand Analysis

$BUMP Utility (Demand) Forecast

We assume that protocol actors are required to stake a fixed 10% of the TVL in $BUMP to be able to gain access to Bumper’s services (i.e. each user is required to bond 10% of the value of their position to access Bumper).

Bumper also has a staking feature, where $BUMP is staked to receive more $BUMP. A target of 30-40% APY is an upper bound APY in the DeFi sector, suggesting a competitive $BUMP reward rate for Bumper’s staking feature.

The bond is categorised as the primary driver of token demand, while the staking feature in conjunction with other secondary market activities will drive speculative demand.

As per the model’s forecast, while the network incentive is a function of TVL, other token emissions are inflating based on a predetermined schedule, such as emissions from vesting. The breakdown of the incentives can be seen in the table below:

Analysis

Underpinning our analysis, we define two key approximations:

Net $BUMP flow is dependent on the demand (both speculative demand and bonding demand) and supply (network incentives and scheduled supply release), and,

The month-on-month market price is a function of the growth rate of net $BUMP flow.

We change in two variables throughout this analysis: speculative demand as a percentage of total demand, and new token supply sell pressure represented by the percentage of new token supply sold.

Our $BUMP price and FDV analysis was constructed around two core premises:

First, we used TVL in the optimisation model as a constraint for $BUMP prices;

Secondly, we used scenario analysis across 2 types of scenarios and 3 cases. Scenario 1 looks at both variables that can be changed, being a) the proportion of speculative demand, and b) degree of selling pressure from vested tokens. Scenario 2 looks at 3 cases: high sell pressure, moderate sell pressure and low sell pressure.

Circulating Supply Analysis

We take a scenario-based approach with Scenario 1 as the ideal scenario that achieves the highest correlation between TVL and BUMP prices, by changing 2 variables.

And, Scenario 2 is the reasonable scenario where we allow speculative demand to change while assuming a BUMP sell rate to be constant. This is by design given that speculative demand is a variable that cannot be controlled by the protocol whereas rate of supply from token holders offering them for sale can be a potential level of coordination among early stage token holders.

Both scenarios show that prices stabilise after the 22nd month, despite the change in tokens sold by users and speculative demand of the token. That shows:

$BUMP is required to be bonded by users to have access to the protocol; and

$BUMP does not accumulate or distribute profits to token holders which would otherwise result in higher premiums and lower yields for Bumper’s users.

Thus, a high correlation between $BUMP prices and TVL of the protocol can be expected and indeed manifests as such in our modelling results.

We allowed iterations in the ratio of speculative demand as a percentage of total demand (being the parameter which impacts total monthly $BUMP demand) and the ratio of supply that are sold (being the parameter that impacts total monthly $BUMP supply) to show a distribution of every possible combination between these two variables between 0 - 100%, before eventually selecting the combination with the highest correlation.

We found that the highest possible correlation (Ideal Scenario) would be achieved with 100% of the new tokens being sold, and 109 times the demand is speculative relative to the internal demand resulting from the bond function.

The result is the price of $BUMP again stabilises at approximately $5.52 around month 22, demonstrating a 90.72% correlation to the TVL.

FDV Analysis

Based on the circulating supply and price analyses above, both prices stabilise at around $5.50, given the changes in fundamental drivers. As a result, the FDV of $BUMP would follow an oscillating trend as shown below, which stabilises around month 15 at $1.35b level by the end of the 3 year analysis.

Specifically, an analysis has also been done to assess the impact of $BUMP price on network incentive and revenue earned by the protocol treasury. To plot these relationships over time, dependent variables were chosen to be presented as a ratio with $BUMP price being the benchmark and denominator.

In terms of the network incentive, the rapid drop in the ratio in month 2 is as a result of the sharp increase in $BUMP market price in the same month. This ratio then gradually decreases as $BUMP price stabilises, and as the protocol reaches a critical level of network effect, and until it reaches 0 in month 25.

On the other hand, treasury revenue has followed a general upward trend over the 3 years. This indicates that the treasury amount increases faster than the rate that the $BUMP price changes. This can be seen at an inverse P/E ratio for the protocol as treasury revenue represents Bumper’s earnings power.

As a result, it can be inferred that the protocol revenue will grow faster than the theoretical valuation via the token and thus result in high FDV. This finding supports our high speculative demand result, but also may be used to reduce protocol fees to further boost internal demand.

Upgrade to the premium newsletter to unlock more content

TLDR:

Above is our analysis of Bumper Finance, a protocol that protects users' assets through a risk conversion mechanism. To do this, we need to design a suitable tokenomics that is enough to incentivise the parties to have certain benefits. Also increases the value of $BUMP and the network over time. After designing tokenomics based on reasonable assumptions, we proceed to evaluate and analyse those variables according to TVL and demand for the protocol. Finally, we have the logical results below:

Cash flow: 528.24% and 174.67% YoY growth

Ecosystem reward based on the Sigmoid Curve: 36.47%, 69.85%, 94.88% YoY emission of the network incentive

Total token emission rate: 22.50%, 11.31% YoY inflation rate.

Token Utility (Demand) Forecast: network incentive would end on month 25. Then, only the protocol’s boost and stake functions would be used to support its future token issuance.

Circulating Supply Analysis: scenario analysis by ideal and reasonable case. Under the reasonable case, 30% of the token supply will be held whereas 70% will be sold, resulting in a long term stabilised price of the $BUMP token at around $5.50.

FDV Analysis: the FDV is high as protocol revenue will grow faster than the theoretical value of the token.