Why Is Algorithmic Stablecoin Important?

Welcome, premium subscribers! Thank you for subscribing. I appreciate you very much. TLDR below. This is not financial advice.

What Is Stablecoin?

Stablecoins are crypto assets that try to reduce volatility by pegging the value to another asset. Thus, it is stable with respect to the asset. For example, the value of the stablecoin will often be anchored to another type of stable asset such as central bank money (USD, CHF, RMB, SGD) or a commodity (gold, silver, precious metals).

Why We Need Stablecoin

Stay tuned for our algo stablecoin research paper coming out! It is a collaboration between Economics Design, Lemniscap VC and Bocconi University.

TLDR: easy access to this new digital crypto space.

Stablecoins appear to solve the biggest problem in the current cryptocurrency market, volatility. For traders or investors, they can convert assets to stablecoins to avoid cryptocurrency volatility without necessarily converting to fiat.

For stores, it is difficult for a company to accept payment with a cryptocurrency when there is a fluctuation of 20-30% in value in a short period of time. This makes the broad adoption of cryptocurrencies much more difficult.

Therefore, stablecoin is important as a bridge between the electronic market and the traditional financial market. The transition from fiat to cryptocurrency has been a lot easier since the advent of stablecoins.

As Erik Voorhees, CEO of Shapeshift said:

“Stablecoins are important in the same way that a bridge is important. You may not care much about the bridge, but without it, the beautiful land beyond is much harder to get to”.

Types Of Stablecoin

How are these stablecoins created? Via various mechanisms which can be broadly classified into fiat-collateralised, crypto-collateralised and algorithmic.

Fiat-Collateralised Stablecoin

This is the most popular form of stablecoin in the cryptocurrency market at the moment. The value of these stablecoins is often pegged to the value of real money at a 1:1 ratio.

The main feature of this type of stablecoin is that the total supply of it on the market must be worth the equivalent of the amount of money stored by the issuer.

To ensure the truthfulness of that, the issuers will be inspected, managed and audited by a reputable financial institution such as a bank or financial audit company.

The risk of this type of stablecoin is the risk that the issuer of the stablecoin cannot prove that the reserve amount is of equal value to the value of the stablecoin circulating in the market.

Some typical fiat-backed stablecoins: Tether ($USDT), TrueUSD ($TUSD), USD Coin ($USDC), Paxos Standard ($PAX).

Crypto-Collateralised Stablecoin

Like fiat-backed, crypto-backed stablecoins are stablecoins that are collateralised by a crypto asset.

However, the difference between these two types of stablecoin is where the collateral is stored.

With fiat-backed, collateral is stored off-chain by reputable third parties such as banks or auditing firms.

With crypto-backed, collateral is stored immediately on blockchain (on chain) which is locked in by means of a Smart Contract. This brings transparency as well as decentralisation.

The risk of the form of stablecoin collateralised by crypto is the fluctuation of the price of the crypto coin that is collateralised.

To minimise that risk, these stablecoins have to increase the value of the collateral to a very high level to ensure that price fluctuations do not affect the stability of the stablecoin.

In case the value of the collateralised crypto is lower than the issued stablecoin, the smart contract liquidates the collateralised assets to ensure the stability of the stablecoin.

Some typical stablecoins: MakerDAO ($DAI), Bitshares ($BitUSD), Celo, Reserves ($RSV).

Algorithmic Stablecoin

This type of stablecoin is not collateralised by any kind of asset. Instead, to maintain stability, these stablecoins use an algorithm-based supply-demand elasticity mechanism.

The working nature of this stablecoin is similar to how central banks work with fiat money.

When the value of a stablecoin is too high due to increased demand, the issuer will bring to the market a quantity of stablecoins until the value of the stablecoin is stabilised.

And vice versa — when the value of the stablecoin drops too low, issuers will issue bonds bought with stablecoins to attract speculators to buy stablecoins. This increases the demand for stablecoin which brings its value back to a stable level.

The risk of this form of stablecoin is that when speculators no longer buy bonds, that stablecoin will collapse. A prime example of this collapse is the Basis Stablecoin.

Some typical stablecoins of this type: Carbon, Steeem Dollar, Bitpay Officical, Nubits.

Stablecoin Benefits

The Market Size

Overall Market

Since the beginning of 2021, stablecoins have seen more than x2.5 growth (from $21.7B peaking at $54.3B), as users continue to have a large demand for stablecoins as a means of storing and converting value on the blockchain.

Source: Messari.io

In the past 1 year, stablecoins have reached a trading volume of nearly $2 trillion and the trend continues to grow. In Q1 2021 alone, the trading volume reached half of the above figure.

Source: stablecoinindex.com

Stablecoins continue to be widely accepted because they are:

Easy to accept;

Based on blockchain 24/7, making them accessible and reliable;

They provide users with greater autonomy, privacy, and compatibility than existing payment solutions that require KYC and restrict access;

They can be used through Dapps. This makes stablecoins even more useful.

Obviously, stablecoins are being used as a means of payment and of convenient value conversion, Exchanges require stablecoins as collateral or designate trading pairs that use stablecoin as the base currency. They are creating real value.

At this point, stablecoins are simply a good means of storing and moving value around the world.

What Is Next?

Stablecoins are one of the few blockchain applications that have a market worth trillions of dollars. With the US dollar accounting for about 55% of the world's international transactions, savings and borrowing, the global demand for $USD are enormous, especially outside of the US financial system.

As discussed, stablecoins are positioned to cater to this need for foreign dollars by providing individuals and businesses around the world with easy access to dollars because they are digital, are globally accessible, and relatively more resistant to seizure.

Problems Of "Old" Stablecoin

The top stablecoins by market capitalisation today are centralised (e.g., USDT) and expose their holders to censorship, seizure, and counterparty risk.

The ability to moderate transactions and seize assets, though reasonable in some cases, is still being sought.

The counterparty risk also affects many of the properties that make blockchain assets unique. Having a stablecoin backed by a single issuer exposes the owner to a potential solvency risk if the issuer encounters any trouble.

The above properties of centralised stablecoins are not only in contrast to those of cryptocurrencies, but, in fact, make them less socially scalable. Social scalability is important, because the more trust is required in the use of stablecoins, the less users trust it for their needs. Decentralisation is not just an ideal. It allows blockchains to be vitally useful to many people and businesses worldwide as it reduces the level of trust required to rely on a system. While not all systems require the attributes of decentralisation, the financial system — and more broadly "money" — requires decentralisation.

Decentralised Stablecoin — $DAI

Fortunately, the industry has created decentralised alternatives. So far, it has received considerable support.

The market-leading $DAI, issued by MakerDAO, has been in operation since December 2017 and has now been in operation for over three years without a major depreciation (it had temporary periods where its peg was slightly reduced). Over its time, $DAI has survived the 2018 bear market, which has seen multiple cryptocurrencies including $ETH crash over 90% and Black Thursday (March 12, 2020) which witnessed many cryptocurrencies go down more than 50% in a day. $DAI is also the most liquid and most widely adopted decentralised stablecoin, available at both CeFi (ex: Coinbase) and DeFi.

Latest good news on $DAI: Maker is moving towards more of a decentralised structure.

Why Do We Need Algorithmic Stablecoins If $DAI Is So Great?

Short Answer: $DAI is not perfect.

To understand why, we need to quickly review how MakerDAO works. It begins with the premise that Maker is a loan protocol and that $DAI is issued as a by-product of loan demand. $DAI is put into circulation through users borrowing with collateral (usually $ETH) that they deposit into Maker's vault. These loans are decentralised to ensure that $DAI is always backed by collateral even if the assets that support the $DAI drop significantly and suddenly. The creator affects the amount of $DAI in circulation, and thus the price of $DAI through the interest charged on loans.

Problems Of $DAI

Maker's model introduces several problems. For one, it is not capital efficient. The fact that you always need more than $1 for every 1 $DAI creates a very capital intensive system and makes it difficult for $DAI to scale on demand. To put it another way, we cannot trade systematic arbitrage when the anchor price of $DAI deviates from $1.

Furthermore, in the same case above, once a user has minted and sold their $DAI, they are still in debt, which they need to pay to get back their collateral. This makes it impossible to trade $DAI spreads in a closed loop like Tether, which offers simple 1:1 conversion for $1 in bank accounts and $USDT.

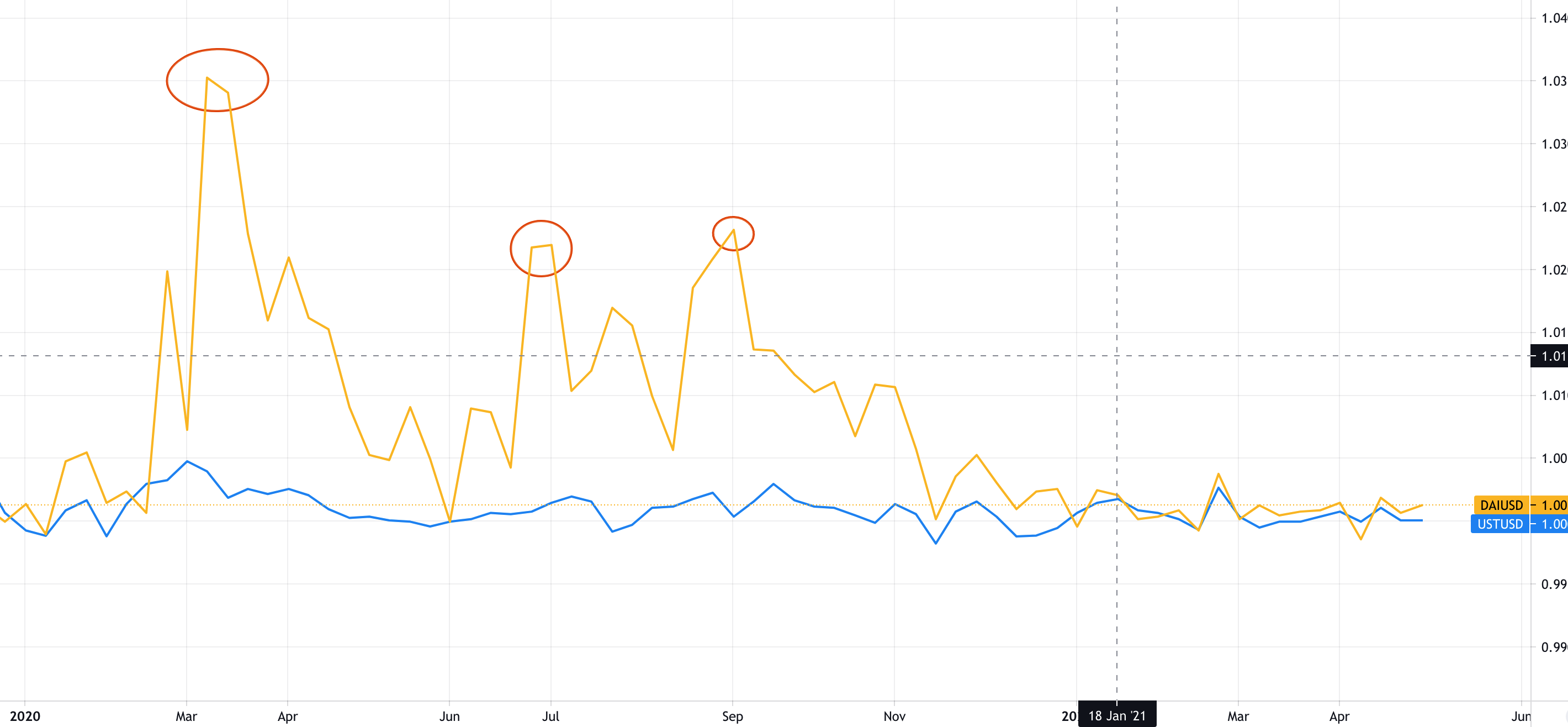

This is not a theory. This is the reality.

On Dark Thursday of March 2020 investors needed $DAI to protect their assets from volatility and to buy $DAI to pay off their Vault (CDP) debt before bankruptcy. The value of $DAI soared as high as 40% from the $1 peg and forced Maker to offer $USDC as collateral to restore the closing price. However, it is still not completely back to the 3-month stellar level.

In addition, yield farming programs caused a spike in demand for $DAI (like $COMP) and also made $DAI higher than the closing level for many months.

The release is not keeping up with demand.

Source: $DAI (Yellow Line) - Tradingview.

The Maker community is well aware of these problems and has since introduced solutions such as its Peg Stability Module. Nowadays $DAI does not expand with demand for $DAI, it expands according to the need for leverage.

Algorithmic Stablecoin Insight

Terra Stablecoin Case

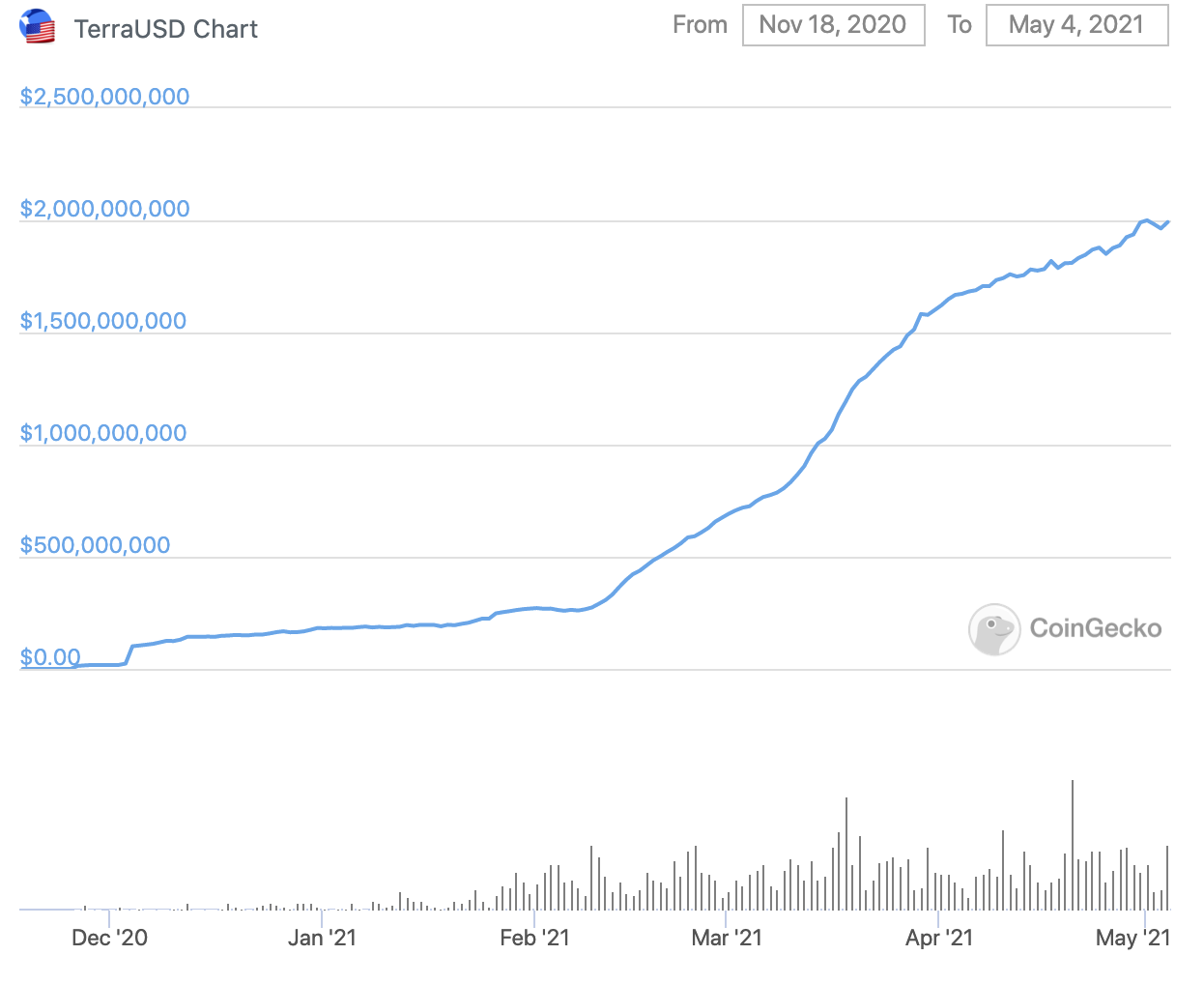

The second promising decentralised stablecoin solution is Terra, an application-specific blockchain built using the Cosmos SDK with the provision of algorithmic stablecoins. Terra's $UST stablecoin has quickly become the second largest decentralised stablecoin in the industry since building a bridge with Ethereum and launching liquidity mining for its new synthetic asset protocol, Mirror.

Terra offers a promising model of providing a capital-efficient, scalable, and decentralised stablecoin. However, it is not perfect either. Terra offers improvements over pure algorithmic stablecoin models, with its $LUNA "share" token having real intrinsic value in the form of Terra transaction fees.

Source: $UST (Blue Line) - Tradingview.

This intrinsic value provides a point of support for the system. Because, in theory, participants would be more willing to burn stablecoins for $LUNA when the stablecoin is below the peg than if the $LUNA was a pure volatility absorption token. But if Terra transaction fees are ultimately the support for Terra stablecoin, it is not sure how much this could increase if Terra's stablecoin growth rate outstrips the Terra transaction fee growth rate issuing $UST every day for this reason).

Source: Marketcap - Coingecko.

Problems Of Algorithmic Stablecoin

Most of today's first-generation algorithm stablecoins such as $ESD, $DSD and Basis Cash are based on the idea of a whitepaper written in 2014 by Robert Sams titled "A Note on Cryptocurrency Stabilisation: Seigniorag." He describes a stablecoin model involving two tokens: one token is a stablecoin and the other acts as a stake in the system's seigniorage (the profits from the new issuance). When the price of the stablecoin > $1 (expansion) and the supply of the stablecoin needs to increase, the new issue will be distributed to the holders of the "stock". When the price of stablecoin falls <$1 (narrow), stablecoins will be removed from circulation by burning them in exchange for new shares. What this model does effectively is divide the system into a speculative asset that absorbs all volatility and a stabilisation asset that is subject to stability.

This model sounds fine but has been challenged in practice recently. The challenge with these models mainly consists of three things:

Bootstrapping system;

Lack of collateral;

Distribution of stablecoins.

Stablecoin Futures

Algo stablecoins are important because they are the next stage to building a decentralised future.

Decentralised Money

Stablecoins are important in the DeFi market because they help with adoption and ease of payment within the system. Stablecoins can be used during a bear market, where the value does not suffer from high volatility. However, current stablecoin models are either kept in centralised custodians (e.g. $USDC, backed by $USD bills facilitated by Coinbase) or backed by on-chain assets, to create debt-backed stablecoins.

The next evolution in decentralised stablecoin is to emulate the central bank's method of creating a currency without debt. This is because there are limitations to debt-backed money, as we have seen in the world when the currency was pegged to gold. There is a limitation to monetary expansion when every dollar is backed by another asset. It is capital inefficient and has a glass ceiling to its expansion.

Central-Bank Like Decentralised Money

That brings us to central-bank like privately issued decentralised money. What we are creating is not just a simple mechanism to achieve a stable pegged value. That can be done with off-chain and on-chain collateral methods as described above.

What we are creating are dynamic mechanisms that allow a stable pegged asset, executed with math and code. And pegging this asset to a stable USD value, which is a test of mechanism design. In the future, true to the philosophy of decentralisation, these mechanisms can be used to peg against a basket of goods, just like central bank money. That is where the true value lies.

This is the greater purpose of creating stablecoins, designed by robust mechanism design.

To understand the importance of decentralised central-bank like mechanism design, we have to understand that this is creating a new infrastructure of base money in its very own economy. Not an economy governed by physical geography or regulatory jurisdiction, but a free-for-all economy, used by everyone and anyone.

TLDR

We are creating dynamic systems and integrating the financial infrastructure into this new system. And this new system can integrate the current policies in place like fractional banking and reserve banking with capital efficiency. The innovation it brings now is dynamic monetary policy and reduced time lag in monetary response. We see an increasing number of papers being written on more robust monetary policies by central banks. They seem novel and to implement them to rewrite the current monetary system is difficult. But with algo stablecoins we can experiment with these designs and study the empirical evidence of their efficiency. In this way we can build better monetary models for the future.

Stay tuned for our algo stablecoin research paper coming out! It is a collaboration between Economics Design, Lemniscap VC and Bocconi University.